IT Audit

An IT audit is the examination and evaluation of an organization's information technology

infrastructure, policies and operations. Information technology audits determine whether

IT controls protect corporate assets, ensure data integrity and are aligned with the

business's overall goals.

Because operations at modern companies are increasingly computerized, IT audits are used to ensure information-related controls and processes are working properly. The primary objectives of an IT audit include:

An IT audit can be defined as any audit that encompasses review and evaluation of

automated information processing systems, related non-automated processes and the

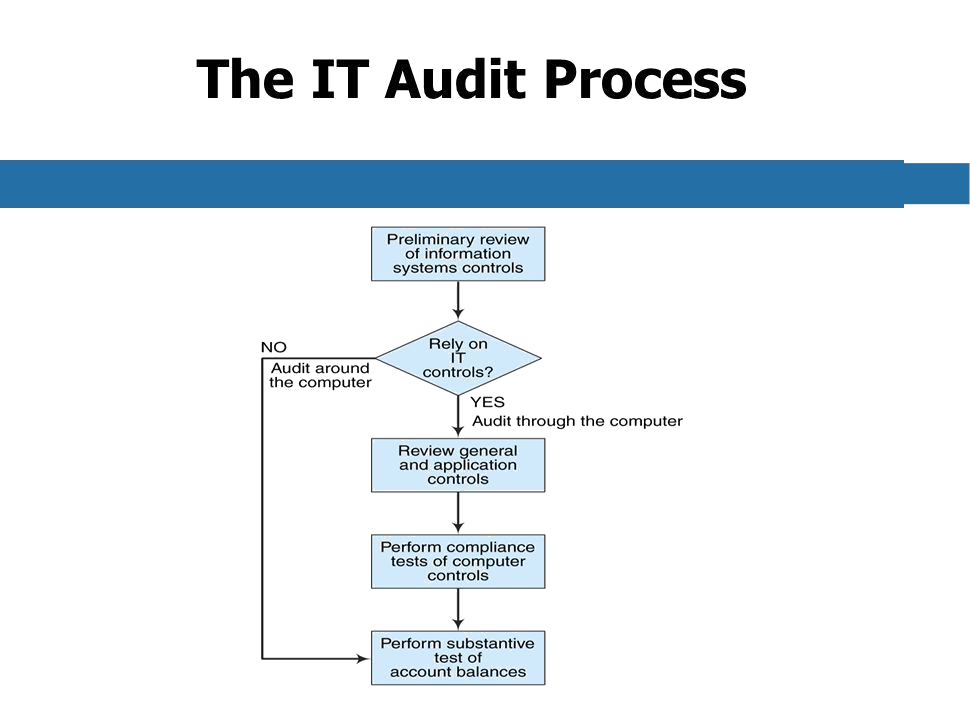

interfaces among them. Planning the IT audit involves two major steps. The first

step is to gather information and do some planning the second step is to gain an

understanding of the existing internal control structure. More and more organizations

are moving to a risk-based audit approach which is used to assess risk and helps an IT

auditor make the decision as to whether to perform compliance testing or substantive

testing. In a risk-based approach, IT auditors are relying on internal and operational

controls as well as the knowledge of the company or the business.

This type of risk assessment decision can help relate the cost-benefit analysis of the

control to the known risk. In the “Gathering Information” step the IT auditor needs to

identify five items:

A side note on “Inherent risks”, is to define it as the risk that an error exists

that could be material or significant when combined with other errors encountered

during the audit, assuming there are no related compensating controls. As an example,

complex database updates are more likely to be miswritten than simple ones, and

thumb drives are more likely to be stolen (misappropriated) than blade servers in

a server cabinet. Inherent risks exist independent of the audit and can occur

because of the nature of the business.

In the “Gain an Understanding of the Existing Internal Control Structure” step, the IT

auditor needs to identify five other areas/items:

Once the IT auditor has “Gathered Information” and “Understands the Control” then they are ready to begin the planning, or selection of areas, to be audited. Remember one of the key pieces of information that you will need in the initial steps is a current Business Impact Analysis (BIA), to assist you in selecting the application which support the most critical or sensitive business functions.